Hydro Leader: Please tell us about your background and how you came to be in your current position.

Matthew Shapiro: I first got interested in the wind energy field in 1990, when I was 22 years old. I started contacting wind developers. At roughly the same time, it occurred to me that with pumped storage, we could store wind energy and create a more dependable product and compete against gas-fired generation, so I started reaching out to independent pumped storage developers and trying to get wind developers interested. At that point, during the 1990s, I was unsuccessful because the market for energy storage was not strong. It really wasn’t on people’s radar screen in relation to renewable energy. But in 2009, seeing that the industry was changing and renewable energy penetration was greatly increasing, I decided to start a company called Gridflex Energy to begin identifying the best new pumped storage sites in the country and building the business case for combining them with renewable energy. In 2019, we formed a partnership with rPlus Energies, a new renewable energy development firm, to form rPlus Hydro.

Hydro Leader: Tell us more about Gridflex Energy and rPlus Energies.

Matthew Shapiro: rPlus Energies is a diversified renewable energy development firm, developing utility-scale solar, wind, and solar plus battery facilities. rPlus Energies is working on a multigigawatt pipeline of projects, separate from the pumped storage side. On the rPlus Hydro side, we’re currently working on 10 projects, which are in different stages of development. They range from 500 to 1,000 megawatts (MW) and are almost all in the western United States, though we do have one project in Kentucky. Eight of them are closed-loop projects, meaning that they don’t involve any existing bodies of water, and two involve existing reservoirs. The two projects farthest along in development are the White Pine Pumped Storage Project, near Ely, Nevada, which is a 1,000 MW closed-loop project, and the Seminoe Pumped Storage Project at Seminoe Reservoir in Wyoming, which is targeted for 900 MW. Most of these projects are sized for 8 hours of full-output storage, though Seminoe is sized for 10 hours. We’ve also filed interconnection applications for several projects, which is a key step in any type of energy storage development.

Hydro Leader: Do you always begin the development process with an entity that will be the ultimate owner or operator of the facility?

Matthew Shapiro: We begin with a good understanding of the market for a project and a target market involving specific utility offtakers. We don’t necessarily begin with agreements in place, but we seek to develop relationships with those potential offtakers. Because we’re going to be investing a large amount of money in project development, we want to know that at the end of the day, there will be a customer. In some cases, those utilities would likely want to own and operate the projects. In other cases, they may continue to be owned and operated by rPlus. It all depends on the market situation.

Hydro Leader: Has the market for new pumped storage hydro projects changed over the last few years?

Matthew Shapiro: Yes. The first generation of pumped storage in the United States was built from the 1960s through the early 1990s. Those projects were all built by utilities or the federal government and were used mainly to shift off-peak nuclear baseload production, which had a low market value, to on-peak periods, when the cost of fossil-fired generation was high. That arbitrage drove the market for all the original projects. Today, the market is driven by the need to store solar- and wind-generated power and make it available when needed. That’s because at the state level—and in some cases, the utility level—a shift is underway to source 50, 80, or 100 percent of energy from renewable generation. That means that you need a way to keep the electrical supply system reliable and stable. In some cases, utilities may still be planning to add a certain amount of gas-fired generation, but those situations are becoming less frequent. If you’re not building fossil generation facilities to keep the system stable, then you need energy storage, and the alternatives for commercialized energy storage available today are few in number. Lithium-ion batteries have advanced and are declining in cost, but pumped storage will be an attractive part of the mix in places where it is developable and where there are good sites.

Hydro Leader: What are some of the biggest challenges in the development of new pumped storage hydro projects?

Matthew Shapiro: First, you need to find outstanding sites, which require a rare combination of characteristics. The basic topography that you’re looking for is a high vertical drop over a short distance with the right geological conditions. A developable pumped storage site must have the right combination of physical features, low to moderate environmental sensitivity, proximity to transmission lines, a source of fill water, and a nearby market.

Development and construction takes roughly 8–10 years, so for current projects, we’re looking at completion in the late 2020s or early 2030s. Once you’ve got a good site, you have to begin the process of engineering, permitting, and licensing. The engineering process is strongly iterative. If most of your features—your powerhouse and your tunnels— are underground, then you have a lot of geotech work to do, which is expensive. It takes time and investment capital to go through the various stages of engineering, one at a time, to better define the cost and the design. Each project is unique. One site may have virtually no land-use or environmental complications. At another site, though, you may uncover a sensitive species or geotechnical complications that you need to work through. Permitting and licensing with the Federal Energy Regulatory Commission (FERC) is a several-year process itself. It involves federal-level reviews—typically an environmental impact statement—as well as additional local and state permitting. If you’re on federal land, you must obtain other permits as well, such as rights of way from the Bureau of Land Management.

It’s a process, and it takes time to de-risk the project and get questions answered. It takes patience to work with the multiple parties that have jurisdiction over a given project site. You need what is referred to as patient capital, and you have to know the development fundamentals of what makes a project real. You have to hit those milestones while at the same time working on your marketing and obtaining market commitments so that there will be a contract at the end of the day. It’s an interesting balancing act—one that relatively few firms are good at or have been willing to undertake.

Hydro Leader: Under what circumstances is a FERC license not required for a pumped storage project?

Matthew Shapiro: There are some circumstances under which your location or project doesn’t trigger any of the jurisdictional factors for FERC licensing. These are sites, for example, that are entirely on private property and don’t involve any headwaters or tributaries of navigable waterways. You can still qualify for FERC licensing on a voluntary path if you desire. We look for that opportunity in unique cases. For one site that we’ve been looking at, we’ve confirmed that a FERC license would not be required if we use groundwater to fill the project, but would be required if we were to buy the water from an agency. It’s an interesting aspect of pumped storage licensing that applies to relatively few sites. We weigh those sites on a case-by-case basis to see if a non-FERC path is worth pursuing.

Hydro Leader: Given that many of the easiest sites for pumped storage projects have been taken, how do you identify new sites?

Matthew Shapiro: It used to be thought that there were no more undeveloped pumped storage sites in the United States. That was completely erroneous. It’s just a matter of cost threshold: The cost profile of one pumped storage site may be $1,500 per kilowatt while that of another may be $3,000 per kilowatt. It’s all driven by the unique features of the location. The size of the project makes a difference as well: There are economies of scale. Having screened hundreds of potential sites across the country, we’ve become quite good at that process, which goes way beyond topography. It requires an understanding of environmental sensitivity, water, transmission, geology, and the market. We are happy with the portfolio we’ve assembled. We may be adding a few other potential sites that involve unique circumstances, such as the Maysville project in Kentucky, which involves an almost vertical drop to a spacious limestone mine 1,000 feet below ground, but those opportunities are rare. There are folks looking at seawater pumped storage, which involves finding a location with a high vertical drop near the ocean and using the ocean as your lower reservoir. Only one has been built, a demonstration product in Okinawa that I believe has since been dismantled. Several other projects involving the creation of an underground reservoir have been proposed. The advantage of that idea is that you could get a high, ideal vertical drop and avoid the environmental impacts of surface construction. On the other hand, the site would have to be ideal from a geological point of view. We don’t have any purely underground projects in our portfolio.

Matthew Shapiro: It used to be thought that there were no more undeveloped pumped storage sites in the United States. That was completely erroneous. It’s just a matter of cost threshold: The cost profile of one pumped storage site may be $1,500 per kilowatt while that of another may be $3,000 per kilowatt. It’s all driven by the unique features of the location. The size of the project makes a difference as well: There are economies of scale. Having screened hundreds of potential sites across the country, we’ve become quite good at that process, which goes way beyond topography. It requires an understanding of environmental sensitivity, water, transmission, geology, and the market. We are happy with the portfolio we’ve assembled. We may be adding a few other potential sites that involve unique circumstances, such as the Maysville project in Kentucky, which involves an almost vertical drop to a spacious limestone mine 1,000 feet below ground, but those opportunities are rare. There are folks looking at seawater pumped storage, which involves finding a location with a high vertical drop near the ocean and using the ocean as your lower reservoir. Only one has been built, a demonstration product in Okinawa that I believe has since been dismantled. Several other projects involving the creation of an underground reservoir have been proposed. The advantage of that idea is that you could get a high, ideal vertical drop and avoid the environmental impacts of surface construction. On the other hand, the site would have to be ideal from a geological point of view. We don’t have any purely underground projects in our portfolio.

Hydro Leader: Have new technologies been developed over the past few years that might make pumped storage projects more feasible?

Matthew Shapiro: The construction methods and technology that were used in the 1960s, 1970s, and 1980s are still quite viable today. The biggest innovation that has occurred in pumped storage is variable-speed pump turbines, which were developed in the 1990s in Japan and have now been used in some 20 plants around the world. Variable-speed motor-generators allow you to have a wider range of operation, primarily in the pumping mode. Fixed-speed units, which are the most common type, already have a wide range of operation in generating mode, but in pumping mode, you’re set at the unit size. With a variable-speed motor, you can vary the pumping significantly and provide a wider range of ancillary services to the grid. That can be attractive in certain markets or under certain circumstances.

Hydro Leader: You talked about the need for financing these projects with patient capital. Have investors shown more interest recently in funding these kinds of projects?

Matthew Shapiro: Our backer for rPlus Hydro and rPlus Energies, the Gardner Company, is one of the largest developers of commercial real estate in the intermountain West. The folks who started that company were concerned about global warming, so they decided to begin investing in renewables. Pumped storage became part of the vision because they recognized the need for storage to provide reliability. The Gardner Company is a particularly visionary group. Some other investors in traditional energy have also stepped into the pumped storage space. Copenhagen Infrastructure Partners purchased a couple of projects under development by Rye Development. NextEra, one of the largest renewable energy firms in the country, got involved with the Eagle Mountain project in California. Several firms have seen the long-term potential of pumped storage and recognize the attraction of investing in projects that have an experienced development team, great sites, and a good market.

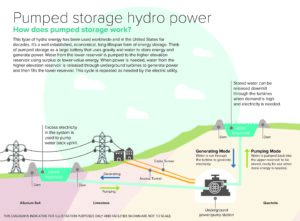

Hydro Leader: What more can you tell us about the importance of pumped storage for the electrical grid?

Matthew Shapiro: In addition to being a firm generating resource, pumped storage is a dispatchable load that can be an important asset for grid stability. The grid currently relies on large rotating machines in the form of fossil fuel generation plants to maintain stability and regulate frequency and voltage levels. As those coal- and gas-fired plants get retired, pumped storage can help fill the need for that type of stability in the system.

It also enables a more efficient use of the transmission that’s delivering renewable energy. For example, wind energy generally has a capacity factor (average generation level) of 35–45 percent. That means new transmission that’s being developed to deliver wind is not really going to be optimally used. But when you add a pumped storage project to the mix, it can help optimally load the transmission by taking surplus off-peak wind and shifting it to times when the wind is not blowing. That’s one of the major drivers for our Seminoe project in Wyoming, which is at the epicenter of Wyoming wind development. That principle applies to solar as well: Pumped storage helps better use the transmission system by being able to absorb and then deliver solar-generated power on demand. Strategically located pumped storage facilities can help manage that grid balancing effectively.

Hydro Leader: Please tell us about your vision for the future.

Matthew Shapiro: I see the transition toward low-carbon or no-carbon resources continuing. Utilities will try to figure out how to make that work while keeping the lights on and keeping the grid stable. It’s widely acknowledged that energy storage will be a major part of the solution. I envision that most, if not all, of the pumped storage developments in our pipeline will become operational, as will several projects that are under development by other firms. The market is quite large. The number of developable pumped storage projects is probably finite, but I think it will be an important part of the mix. I think more and more utilities are realizing that, and I think that for the first time since the early 1990s, we will see several new pumped storage projects come into operation around the end of this decade and the beginning of the next.

Matthew Shapiro is the CEO of rPlus Hydro. He can be contacted at mshapiro@rplushydro.com.